United to House LA (UHLA) is the group behind the Measure ULA real estate transfer tax. Yesterday they shared a press release touting findings from a new analysis of the tax by BAE Urban Economics, investigating whether an exemption for recently completed multifamily and commercial developments (as Jason Ward and I argue for here) would boost production in Los Angeles. I assume the analysis was commissioned by UHLA or an allied group, but I couldn’t find the attribution in the report or press release. (Happy to revise this if I’ve just missed it.)

They conclude that the waiver wouldn’t do much to restore multifamily construction in the city. As the press release puts it, “the proposal before the Los Angeles City Council to waive ULA for any construction newer than 15 years would make very few projects feasible, and instead simply give a subsidy to projects that are already feasible.”

The credibility of that conclusion rests, of course, on the quality of BAE’s analysis. In my opinion, it is quite bad. This probably won’t be my final word on the report, which I’ve yet to read in its entirety, but below are some initial thoughts on where it falls short and how its findings are already being misinterpreted or misrepresented.

1. They ignore how the Lewis Center/RAND reports isolate the effect of Measure ULA on property sales with a quasi-experimental research design.

One of the report’s main claims is that most development projects would be infeasible right now with or without ULA, due to high interest rates, plateauing or declining rents, etc. That's presented as a counter to our research findings in Taxing Tomorrow, but Jason and I never claimed otherwise. We found that the tax was reducing sales of properties with high redevelopment potential above and beyond reductions seen in other LA County cities, and that the drop in sales in Los Angeles was linked to a drop in multifamily permitting on exactly those kinds of parcels.

Throughout the BAE report they point to how 2020-2023 (the pre-ULA period) was a wild time, which it was. But it was wild throughout the county (and state, and nation, and world), and we show that sales trends for properties above and below the ULA eligibility threshold showed almost exactly the same trends inside and outside of the city. After ULA went into effect, the trends inside and outside LA kept tracking each other below the ULA threshold, for property sales that don’t pay the tax, but they sharply diverged above the threshold. So that aspect of their analysis seems irrelevant, at least if this is intended to refute our findings.

2. They draw sweeping conclusions from a tiny set of feasibility scenarios.

The BAE report states that fewer multifamily projects would be financially feasible today compared to 2-3 years ago even if Measure ULA had never been approved. I agree. Los Angeles can't do anything about interest rates; that's up to the Federal Reserve.

But that's not the relevant question. The question is, or should be, whether ULA is making matters worse, and the BAE report appears carefully designed to arrive at "no” for its answer.

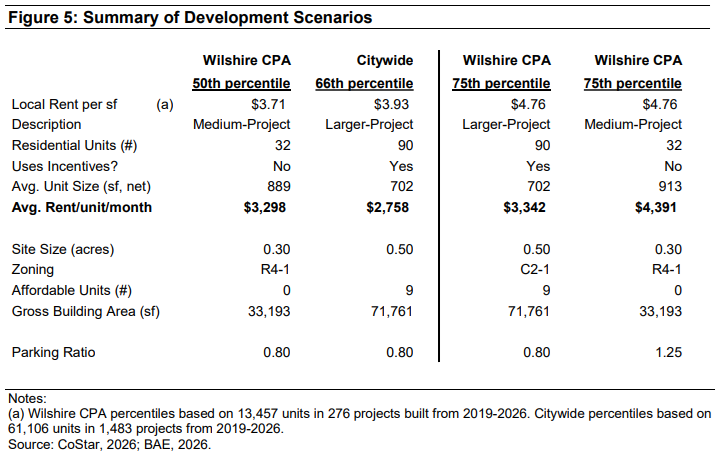

The most salient fact is that they evaluate just two multifamily building types (32 units and 90 units) in one community plan area (of the city's 34). The building characteristics are described in Figure 5 below. From the analysis of these two buildings in one neighborhood, United to House LA is able to say that a 15-year exemption “would make very few projects feasible.” (This is less important, but for some reason, the smaller building doesn't use density bonus incentives — nearly unheard of in today's development environment.)

They find that neither project is feasible at 50th or 66th percentile asking rents, with or without ULA, and that both are feasible at 75th percentile rents, also with or without ULA, depending on how long the building is held before selling. The obvious question to ask is: What about a project that rents at the 70th percentile, or the 72nd?

Somewhere between these scenarios they've selected is a project that is infeasible with ULA and feasible without — I'm sure BAE would acknowledge as much. And that's what we're concerned with: the effect of the tax on the marginal project, the one that would've happened but for Measure ULA. We found that there are likely at least a few thousand such units per year that fall into that category. That's a lot, and it will have an effect on housing affordability and availability in the city and region, but it's still only about 15-20% of the multifamily units permitted during LA's most recent peak in 2022.

3. They don’t address the impact of the tax on residual land value and land acquisition.

We've noted in our writing that Measure ULA's effect on multifamily production may often come down to land acquisition — it's one reason our study focuses on the sale of land with high redevelopment potential. If I'm a developer planning to buy a parcel of land for $6 million, build apartments on it, and sell the project for $30 million, then I need to somehow offset the $1.65 million ULA tax I'll pay at the end. The most realistic way to do that is by paying less for land.

But if I can now only pay $4.35 million for land, and it's got an office building on it worth $5 million to some commercial investor, then they're going to win the bid for that property and no homes are getting built. Or maybe it's got an office on it that's only worth $3 million but the landlord is set on getting $6 million for it or he won't sell; once again, no new housing. As far as I can tell, they don't account for these possibilities at all.

4. The stuff about holding periods is strange and, frankly, naive.

I'll admit that I don't entirely follow BAE’s focus on the holding period, which is the time between finishing construction and selling the building. For many developers that sale takes place within a few years of opening up, after the building is fully leased up or “stabilized.”

Their argument seems to be that if developers just held onto buildings longer before selling, then Measure ULA would be less of a problem for them. That may very well be true, but that's not everyone's business model and it strikes me as quite weird for a real estate consultancy to imply that developers could just arbitrarily change their business model in such dramatic fashion.

Building, leasing up, and selling is a common multifamily development business model across the US, and while I'm not sure I'd say it's "better" or "worse" than holding for longer, it does have the advantage of allowing investors to redeploy their capital to build their next project more quickly. If they can't do so, that could reduce housing production in an entirely different way, as capital is increasingly tied up in buildings completed, 3, 5, 10 years ago.

At one point they also describe the build, lease-up, sell model as "creating and flipping properties." Flipping has a very different meaning than buying land, erecting an apartment on it, and selling it. Just very, very odd. It seems to be intended to problematize a totally normal business activity.

5. Whether or not it’s intentional, some of the framing invites readers to mis/over-interpret the report’s findings.

They say, for example, "For tested scenarios that do not generate a positive return-on-cost ... waiving the ULA tax alone is not sufficient to help the projects achieve a target IRR threshold" and "For the smaller share of tested scenarios that do generate a positive return-oncost, waiving the ULA tax is not needed to help the projects achieve a target IRR threshold..."

The way this is presented makes it easy for the casual reader to interpret the findings as something like "There aren't any infeasible projects that would be made feasible by waiving the tax." That's unfortunate because it's not the correct conclusion to draw from this analysis, and I suspect it’s not a conclusion the report's authors would endorse.

6. Their analysis of the share of multifamily and commercial transactions that are recently-completed buildings arguably makes a case for a waiver.

Here’s the first figure from the report:

I think its purpose is to suggest that Measure ULA is no big deal because over 80% of units in ULA-eligible multifamily transactions are in projects over 10 years old. If so, it's the wrong chart for that claim. LA's housing stock grows by around 1.5% per year or less, so of course most sales are going to be of older multifamily — the vast majority of the stock is over 10 years old.

If anything, this chart seems to suggest (as our own research does) that exempting recently completed projects from the tax would have only a small impact on ULA revenues. And if multifamily production stays depressed, the share of revenues coming from newer building sales may fall even more in the future. In that case we’d be in a lose-lose scenario in which the tax is reducing housing production and isn’t raising any revenue from new projects because no one’s building them.